Shareholder Loan Repayment Journal Entry. Debit cash in bank (or wherever the funds were deposited. To record the repayments you’ve made:

The Road to PPP Loan — Black Bookkeeping from www.blackbookkeepingllc.com

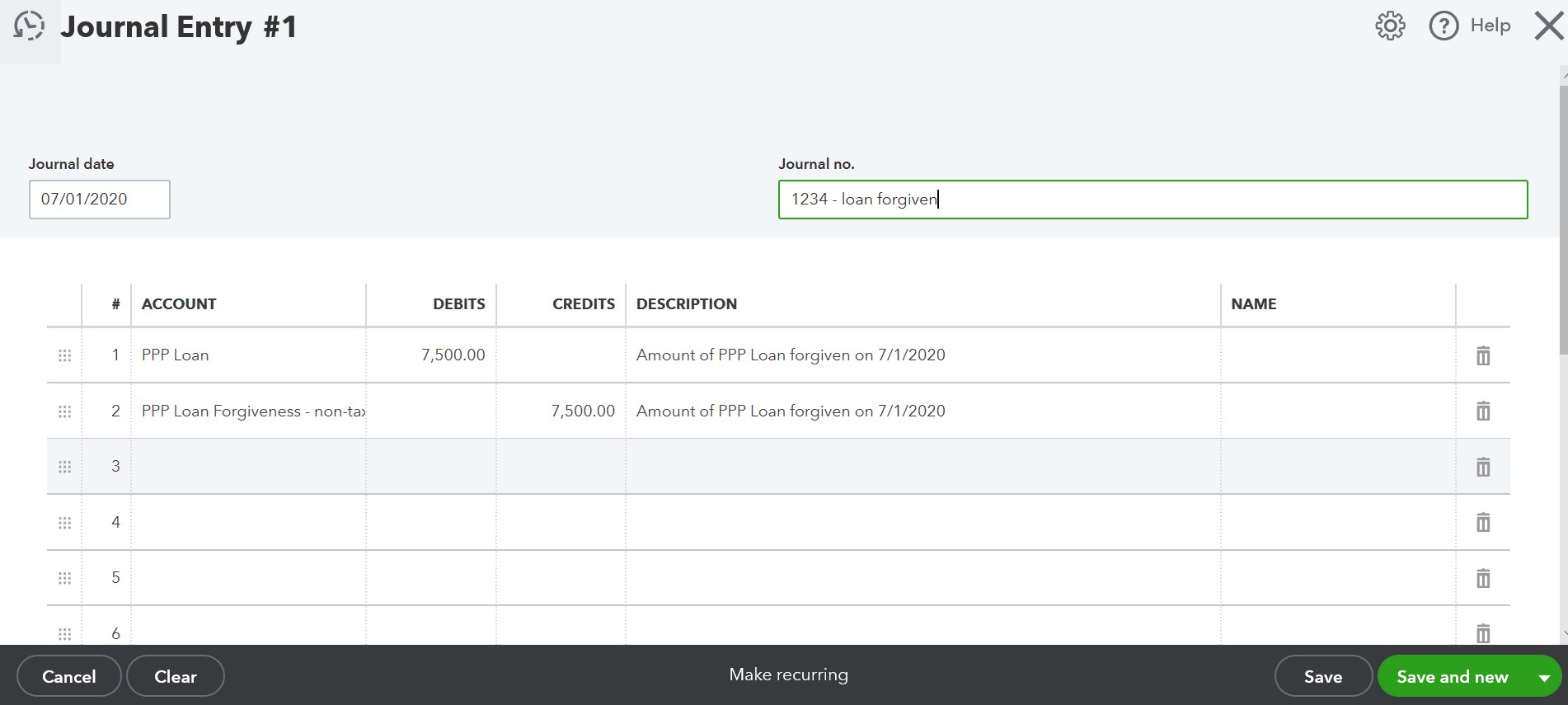

The other side of this entry is credit to other income often described as debt forgiveness in the profit and loss. Using journals to make div 7a loan repayments. Through a bank transaction reconciliation:

Accountants Also Record Debits To Loans.

The shareholder should try to make actual payments with regards the loan and not journal entries. The loan is a liability for the borrower which is a credit balance on the balance sheet. These represent repayments made against the loan.

For Whatever Reason, Y Sells The Loan (The Asset, L) To X.

Journal entry when the repayment is made. Assets increase on the debit side (left side) and decrease on the credit side (right side). Your journal entry to setup your long term shareholder loan would be:

Practitioners Are Urged To Be Careful When It Comes To Complying With Rules Governing The Payment Of A Dividend By Journal Entry To Make A Minimum Yearly Repayment On A Complying Division 7A Loan.

Cr loan from shareholder $1000 (clears the shareholder loan) dr dividends payable $1000 (increases dividends payable) cr dividends payable $1000 (clears dividends payable) dr retained earnings $1000 (reduces retailed earnings accordingly) thanks in advance. Click the add transaction drop down and under money in, select deposit from other accounts. Under other, select journal entry.

In Order To Make The Loan Repayment Journal Entries It Is Necessary To Split Each Of The Cash Payments Into The Principal And Interest Elements As They Are Posted To Different Accounts.

Select the from account as the loan account you had created. The shareholder loan was made to you or your spouse to buy a home to inhabit, and you received the loan in your capacity as an employee of the corporation, and bona fide arrangements are met.*; The other side of this entry is credit to other income often described as debt forgiveness in the profit and loss.

Of All The Above Issues & Factors, Perhaps The Most Important Is Whether Or Not The Shareholder Was Actually Repaying The Loan.

A loan journal entry can be recorded in different ways in bookkeeping software, here are three of them: They can be obtained from banks, nbfcs, private lenders, etc. Now the journal entry for repaying the loan is as follows: