Purchases Debit Or Credit In Trial Balance. Assets, liabilities, equity, dividends, revenues, and expenses. Opening stock/closing stock rent, printing & stationary, salaries etc.

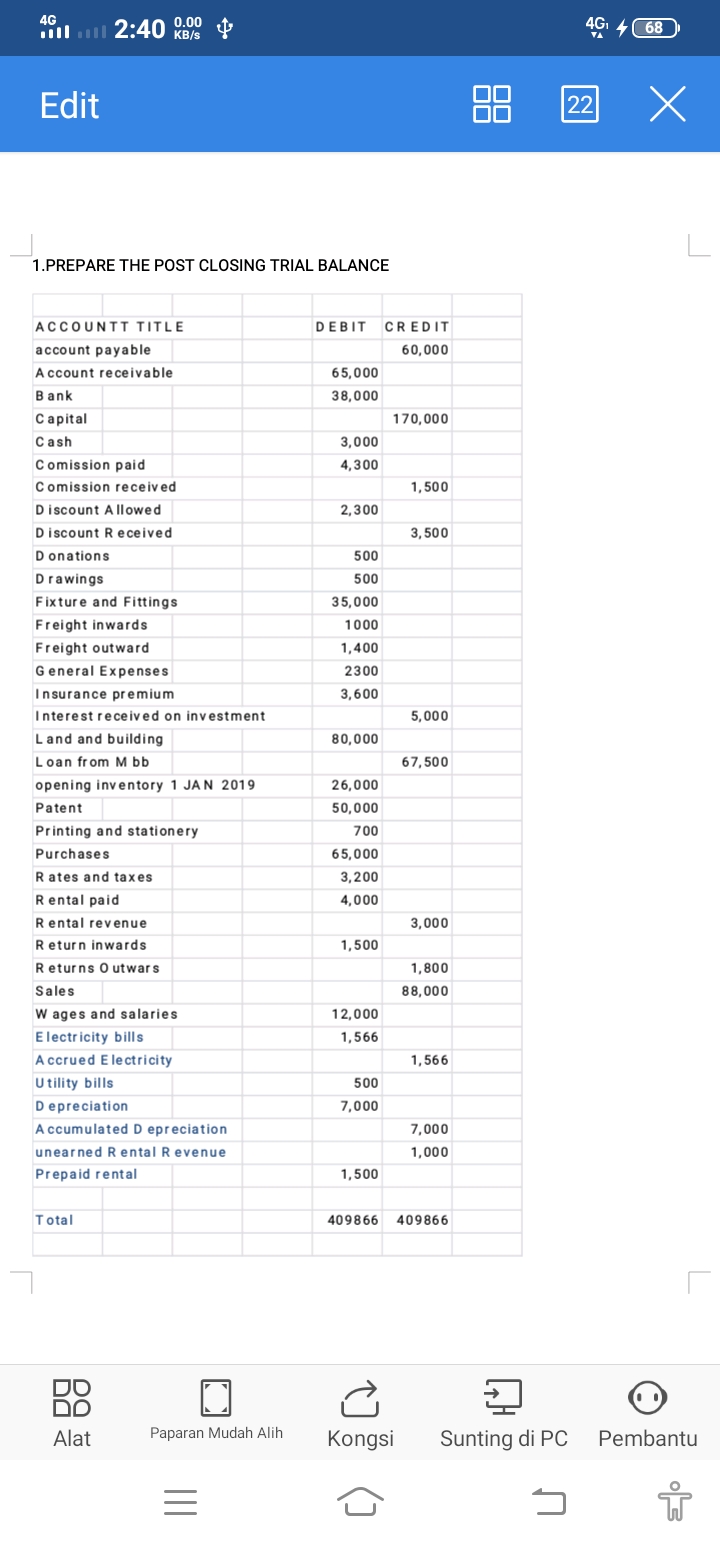

Answered 1.PREPARE THE POST CLOSING TRIAL… bartleby from www.bartleby.com

In addition, it should state the final date of the accounting period. All expenses and losses must be on the debit side. It is usually prepared at the close of the accounting cycle to validate the arithmetical consistency of the records in the ledger before the actual accounts are.

To Put It Simply, A Trial Balance Is A Detailed List Of All The Nominal Ledger (General Ledger) Accounts Contained In The Ledger Of A Business.

If you miss any detail, it might result in a loophole in the ledger. Assets, drawings, expenses & loses credit balances: Mcqs chapter 6 trial balance and rectification of errors have been prepared by our team of best accountancy teachers.

Purchase Of Goods Is Treated As Expense And Purchases Was Made Against Cash Which Reduces Cash.

(if an account has a zero balance, it may be included in the trial balance with zero in the column for its normal balance). Trial balance of a bookkeeper shows an excess of debits over credits by ` 261. Purchases are an expense which would go on the debit side of the trial balance.

This Difference Is Placed In A Suspense Account To Facilitate Books Closure.

Loans given preliminary expenses sales returns p & l a/c (loss) trial. All liabilities must be on the credit side. Trial balance as at 31 december $ $ bank 1,000 wages 300

Also, Is Purchases Included In Trial Balance?

It is usually prepared at the close of the accounting cycle to validate the arithmetical consistency of the records in the ledger before the actual accounts are. ‘purchases returns’ will reduce the expense so go on the credit side. Assume that ending inventory is $8,000.

That Is Increase Or Decrease In Stock Value In Current Period End Is Credited Or Debited To The Opening Stock Account.

That is increase or decrease in stock value in current period end is credited or debited to the opening stock ac. The trial balance can be drawn in the below two forms. The difference between the debit and credit totals is put into a suspense account in the smaller of the two columns.